Our Main Office

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Thu June 15, 2017 - National Edition

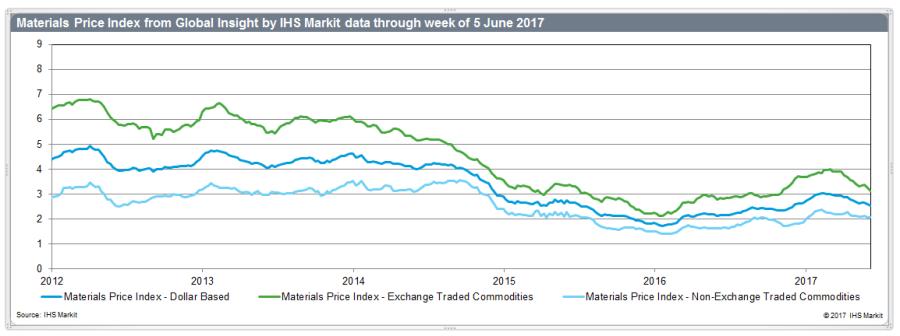

The Materials Price Index (MPI) lost another 2.4 percent last week, taking its cumulative fall over the last four months to 17 percent. For a second consecutive week, the MPI's retreat was broad-based, with nine of 10 sub-indexes declining. Oil and rubber prices once again led the retreat, down 4.5 percent and 13.6 percent, respectively. Only pulp prices rose, moving up 2.8 percent.

Natural rubber prices have dropped by one-quarter over the last two weeks, reaching a low point for 2017. An end to seasonal rains and the release of stockpiled inventory have improved the supply picture while concern over Chinese car sales have undercut the demand outlook. The combination has sent prices tumbling. Alongside oil and rubber, ferrous prices also were down sharply, with the sub-index slipping 4.0 percent as iron ore prices continue to slide on Chinese steel production fears.

More generally, growing worries about oversupply continue to swirl around commodity markets. Last week's macroeconomic announcements do indicate global industrial activity is holding up well, although the mood is no longer as bright as it was a few months ago. Markets in the United States and Europe are seeing moderate growth; however, it is Asia, and especially China, where markets are focused. For China, there is the growing realization that the second half of the year may not match the first six months of 2017. There also is the feeling that U.S. stimulus in the form of tax cuts and infrastructure funding may be delayed. The net result is that some of the optimism priced into commodities late last year is now coming back out of markets.

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Construction Equipment Guide covers the nation with its four regional newspapers, offering construction and industry news and information along with new and used construction equipment for sale from dealers in your area. Now we extend those services and information to the internet. Making it as easy as possible to find the news and equipment that you need and want.

Contents Copyrighted 2024, by Construction Equipment Guide, which is a Registered Trademark, registered in the U.S. Patent Office. Registration number 0957323. All rights reserved, nothing may be reprinted or reproduced (including framing) in whole or part without written permission from the publisher. All editorial material, photographs, drawings, letters, and other material will be treated as unconditionally assigned for publication and copyright purposes and are subject to Construction Equipment Guide’s unrestricted right to edit and comment editorially. Contributor articles do not necessarily reflect the policy or opinions of this publication.

Read our privacy policy here.

Mastodon