Our Main Office

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Tue February 21, 2017 - National Edition

Fourth Quarter and 2016 Breakdown

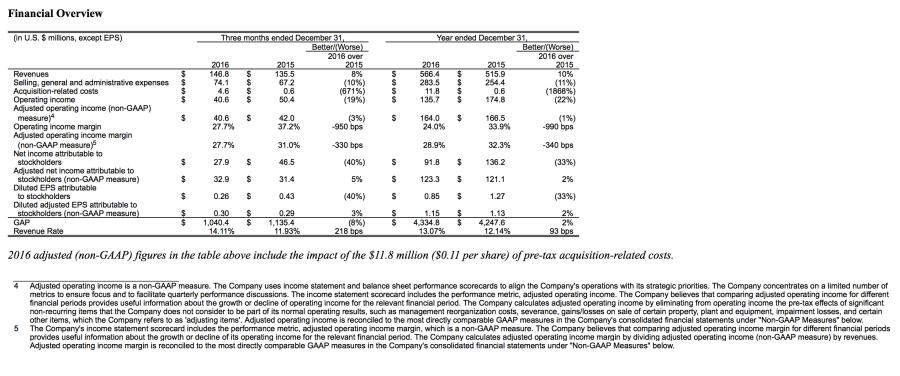

Ritchie Bros. Auctioneers Incorporated (NYSE & TSX: RBA, the "Company" or "Ritchie Bros.") reports results for the three months and year ended December 31, 2016.

During the fourth quarter, the Company generated $146.8 million of revenue, an 8% increase compared to revenues of $135.5 million in the fourth quarter last year, and net income attributable to stockholders for the fourth quarter of $27.9 million, a 40% decrease compared to the record $46.5 million of net income attributable to stockholders earned in the same period last year. There were a number of non-recurring events that affected Ritchie Bros.' fourth quarter results in 2016 and 2015. Included in the fourth quarter 2016 results were $6.8 million of pre-tax ($5.0 million of after-tax) expenses related to the early termination of pre-existing long-term debt due to recapitalization activities. The year ago quarter, Q4 2015, benefited from the after-tax impact of $15.2 million of non-recurring events. Removing these non-recurring events, adjusted net income attributable to stockholders (non-GAAP measure) during the fourth quarter of 2016 was $32.9 million, a 5% increase compared to $31.4 million in Q4 2015.

Diluted earnings per share ("EPS") attributable to stockholders during the fourth quarter was $0.26, a 40% decrease compared to diluted EPS attributable to stockholders of $0.43 in the fourth quarter of 2015. Adjusted EPS attributable to stockholders3 (non-GAAP measure) during the fourth quarter of 2016 was $0.30, a 3% increase compared to $0.29 in the year ago quarter. $4.6 million of before-tax acquisition-related costs are included in both GAAP and adjusted (non-GAAP) fourth quarter 2016 results.

During the year ended December 31, 2016, the Company generated $566.4 million of revenue, a 10% increase compared to revenue of $515.9 million in 2015. Net income attributable to stockholders during 2016 was $91.8 million, a 33% decline compared to $136.2 million in 2015, and diluted EPS attributable to stockholders was $0.85 in 2016, a 33% decrease relative to $1.27 in 2015. Included in Ritchie Bros.' 2016 results were a $26.4 million ($28.2 million pre-tax), non-cash impairment charge related to EquipmentOne goodwill and customer relationships and a $5.0 million ($6.8 million pre-tax) charge related to the early termination of pre-existing debt. Removing the impact of these non-recurring items, adjusted net income attributable to stockholders (non-GAAP measure) for 2016 was $123.3 million, a 2% increase from adjusted net income of $121.1 million in 2015.

Diluted adjusted EPS attributable to stockholders (non-GAAP measure) for the year ended December 31, 2016 was $1.15, a 2% increase from $1.13 last year. Included in both the Company's GAAP and adjusted (non-GAAP) 2016 results were $11.8 million of before-tax acquisition-related costs.

"In 2016, we laid a strong foundation to accelerate Ritchie Bros.' growth trajectory through several acquisitions, including Mascus, the premier listing service in Europe; Kramer Auctions, a regional agricultural auctioneer in Canada; Petrowsky Auctioneers, an industrial auctioneer in the U.S. North East; and acquired 100% ownership of Ritchie Bros. Financial Services. Importantly, we announced the landmark acquisition of IronPlanet, a leading online equipment marketplace and a strategic alliance with Caterpillar. Collectively, these initiatives are transforming Ritchie Bros. into a significant multichannel player with the unique ability to be a one-stop-shop solution provider to customers for their various asset management and disposition needs," said Ravi Saligram, CEO, Ritchie Bros.

Mr. Saligram added: "Despite equipment pricing volatility during the year and management's focus on acquisition activity, I am proud that our team delivered solid business results in 2016 – highlighted by a 10% increase in revenue and an all-time record annual revenue rate of 13.07%. Our 2016 operational metrics were also strong, with the number of consignors, lots, and buyers all increasing 12% versus prior year – further strengthening our network effect. Our diversification strategy is also working, as evidenced by our record quarterly revenue rate of 14.1% in Q4 2016, which was driven by both strong core business performance, and revenue streams from new businesses and channels."

1

Revenue Rate is calculated as revenues divided by Gross Auction Proceeds ("GAP"). GAP represent the total proceeds from all items sold at the Company's auctions and online marketplaces. GAP is not a measure of financial performance, liquidity, or revenue, and is not presented in the Company's consolidated financial statements.

2

Adjusted net income attributable to stockholders is a non-GAAP financial measure. The Company believes that comparing adjusted net income attributable to stockholders for different financial periods provides useful information about the growth or decline of our net income attributable to stockholders for the relevant financial period, and eliminates the financial impact of adjusting items the Company does not consider to be part of its normal operating results. Adjusted net income attributable to stockholders represents net income attributable to stockholders excluding the effects of adjusting items and is reconciled to the most directly comparable GAAP measures in our consolidated financial statements under "Non-GAAP Measures" below.

3

Diluted adjusted EPS attributable to stockholders is a non-GAAP financial measure. We believe that comparing diluted adjusted EPS attributable to stockholders for different financial periods provides useful information about the growth or decline of the Company's diluted EPS attributable to stockholders for the relevant financial period, and eliminates the financial impact of adjusting items we do not consider to be part of the Company's normal operating results. Diluted adjusted EPS attributable to stockholders is calculated by dividing adjusted net income attributable to stockholders (non-GAAP measure) by the weighted average number of dilutive shares outstanding. Diluted adjusted EPS attributable to stockholders is reconciled to the most directly comparable GAAP measures in the Company's consolidated financial statements under "Non-GAAP Measures" below.

Results of operations – Fourth Quarter Update

For the three months ended December 31, 2016

GAP was $1,040.4 million for the fourth quarter of 2016, an 8% decrease compared to the fourth quarter of 2015. This decline is due mostly to auction timing differences and used equipment values. Lot count (auction volumes) declined 3% in the fourth quarter of 2016 relative to the fourth quarter of 2015.

EquipmentOne, the Company's online equipment marketplace, contributed $40.6 million of gross transaction value ("GTV")6 to GAP in the fourth quarter of 2016, a 12% increase compared to $36.1 million in the fourth quarter of 2015. Foreign exchange rates did not have a significant impact on GAP in the fourth quarter of 2016.

Revenues increased 8% during the fourth quarter of 2016 to $146.8 million, compared to $135.5 million in the fourth quarter of 2015, primarily due to a stronger (record) Revenue Rate, which benefitted from robust underwritten contract performance and a growing revenue contribution from new fee-based revenue streams compared to the relative quarter last year. Foreign exchange rates did not have a significant impact on revenues in the fourth quarter of 2016.

The Revenue Rate for the fourth quarter of 2016 was a record 14.11%, compared to 11.93% in the fourth quarter of 2015. The increase in the Revenue Rate is primarily due to the performance of the Company's underwritten contracts combined with an increase in fee revenue, which is not directly linked to GAP. During the fourth quarter of 2016, the Company continued to actively pursue the use of underwritten commission contracts from a strategic perspective, entering into such contracts only when the risk/reward profile of the terms were agreeable. The Company's underwritten contract volume decreased to 26% of GAP during the three months ended December 31, 2016 compared to 29% in the same period in 2015. Straight commission contracts continue to account for the majority of GAP.

Selling, general and administrative ("SG&A") expenses were $74.1 million during the fourth quarter of 2016, a 10% increase compared to the same period last year. Higher staffing levels and new executive roles relative to the comparable period were the largest increases to SG&A expenses. Mark-to-market fair value changes in the Company's liability-classified share units accounted for $1.3 million of the $6.9 million increase. Petrowsky and Mascus accounted for another $0.8 million and $0.5 million, respectively. The remainder of the increase is primarily attributable to our value-added service offerings, and in particular, the costs required to support the growing fee revenues generated by that business.

Acquisition-related costs totaling $4.6 million were booked during the fourth quarter of 2016, compared to $0.6 million in the fourth quarter of 2015. Fourth quarter 2016 costs primarily related to integration planning and legal activities for the announced acquisition of IronPlanet, as well as continuing employment costs incurred to retain key employees for a specified period of time following the Company's business acquisitions. Fourth quarter 2015 costs relate entirely to the acquisition of Xcira. These costs are in addition to SG&A expenses.

Operating income decreased 19% during the fourth quarter of 2016 to $40.6 million, compared to $50.4 million in the fourth quarter of 2015. This decrease is primarily due to a reduction in the gain on disposal of property, plant and equipment, combined with increases in SG&A expenses, acquisition-related costs, and foreign exchange losses, partially offset by the increase in revenues. Adjusted operating income (non-GAAP measure) decreased 27% during the fourth quarter, to $30.5 million, from $42.0 million in the same period last year. Foreign exchange losses that occurred in both the fourth quarter of 2016 and 2015 are now reported in operating income, per US GAAP. They did not have a significant impact on operating income in the fourth quarter of 2016.

Operating income margin, calculated as operating income divided by revenues, was 27.7% for the fourth quarter of 2016, 950 basis points lower than 37.2% for the same period last year. This decrease is primarily due to a reduction in the gain on disposal of property, plant and equipment, combined with increases in SG&A expenses, acquisition-related costs, and foreign exchange losses, partially offset by the increase in revenues. Adjusted operating income margin (non-GAAP measure) decreased 330 bps to 27.7% in the fourth quarter of 2016 from 31.0% in the fourth quarter of 2015.

Net income attributable to stockholders decreased $18.7 million, or 40% to $27.9 million in the fourth quarter of 2016 compared to $46.5 million in the fourth quarter of 2015. This decrease is primarily due to non-recurring events in the fourth quarter last year, including tax loss savings and gains on the sale of excess property. Adjusted net income attributable to stockholders (non-GAAP measure) increased $1.5 million, or 5%, to $32.9 million in the fourth quarter of 2016 from $31.4 million in the fourth quarter of 2015.

Diluted earnings per share attributable to stockholders for the fourth quarter of 2016 was $0.26, a 40% decrease compared to $0.43 in the fourth quarter of 2015. This decrease is primarily due to non-recurring events in the fourth quarter last year. Diluted adjusted EPS attributable to stockholders (non-GAAP measure) increased 3% to $0.30 per share in the fourth quarter of 2016 from $0.29 per share in the fourth quarter of 2015.

6

GTV represents the total proceeds from all items sold at the Company's online marketplaces. In addition to the total value of the items sold in online marketplace transactions, GTV includes a buyers' premium component applicable only to the Company's online marketplace transactions. It is not a measure of financial performance, liquidity, or revenue, and is not presented in the Company's consolidated financial statements.

Results of operations – full year 2016

for the year ended December 31, 2016

GAP was $4.3 billion in 2016, a 2% increase compared to 2015. EquipmentOne, the Company's online equipment marketplace, contributed $148.0 million of GTV to GAP during 2016, a 23% increase compared to $120.0 million in 2015. Foreign exchange rates did not have a significant impact on GAP in 2016.

Revenues grew 10% in 2016 to $566.4 million, compared to $515.9 million in 2015, primarily due to a stronger (record) Revenue Rate, which benefitted from robust underwritten contract performance and a growing revenue contribution from new fee-based revenue streams compared to last year. Foreign exchange rates did not have a significant impact on revenues in 2016.

The Revenue Rate was 13.07% in 2016, compared to 12.14% in 2015. The increase in the Revenue Rate is primarily due to the performance of the Company's underwritten contracts combined with an increase in fee revenue, which is not directly linked to GAP. The Company's underwritten contract volume decreased to 25% of GAP during 2016 compared to 29% in 2015. Straight commission contracts continue to account for the majority of GAP.

SG&A expenses were $283.5 million during 2016, an 11% increase compared to the same period last year. Higher staffing levels and new executive roles relative to the comparable period were the largest increases to SG&A expenses. Mark-to-market fair value changes in the Company's liability-settled share units accounted for $6.3 million of the $29.1 million increase. Mascus, Xcira, and Petrowsky accounted for another $4.8 million, $2.7 million, and $1.2 million, respectively. The remainder of the increase is primarily attributable to our value-added service offerings, and in particular, the costs required to support the growing fee revenues generated by that business. Foreign exchange rates did not have a significant impact on SG&A expenses in 2016.

Acquisition-related costs totaling $11.8 million were booked during 2016, compared to $0.6 million in 2015. $8.2 million of the 2016 costs relate to integration planning and legal activities for the announced acquisition of IronPlanet. $2.5 million of the 2016 costs consist of continuing employment costs, which compares to $0.2 million in 2015. These costs were incurred to retain key employees for a specified period of time following the Company's business acquisitions.

An impairment loss of $28.2 million (non-cash) was recognized in 2016 on the EquipmentOne reporting unit goodwill and customer relationships (the "EquipmentOne impairment loss") as a result of the identification of an indicator of impairment during the third quarter of 2016. The indicator of impairment consisted of a decline in actual and planned revenue and operating income compared with previously projected results.

Operating income decreased 22% in 2016 to $135.7 million, compared to $174.8 million in 2015. This decrease is primarily due to the EquipmentOne impairment loss combined with increases in SG&A expenses, acquisition-related costs, and costs of services, as well as a reduction in the gain on disposal of property, plant and equipment, partially offset by the increase in revenues. Adjusted operating income (non-GAAP measure) decreased 1% during 2016, to $164.0 million, from $166.5 million in 2015. Foreign exchange losses did not have a significant impact on operating income in 2016.

Operating income margin was 24.0% in 2016, 990 basis points lower than 33.9% last year. This decrease is primarily due to the EquipmentOne impairment loss combined with increases in SG&A expenses, acquisition-related costs, and costs of services, as well as a reduction in the gain on disposal of property, plant and equipment, partially offset by the increase in revenues. Adjusted operating income margin (non-GAAP measure) decreased 340 bps to 28.9% in 2016 from 32.3% in 2015.

Net income attributable to stockholders decreased $44.4 million, or 33%, to $91.8 million in 2016 compared to $136.2 million in 2015. This decrease is primarily due to non-recurring events in both years, including the EquipmentOne impairment loss, tax loss savings, gains on the sale of excess property, and debt extinguishment costs. Adjusted net income attributable to stockholders (non-GAAP measure) increased $2.2 million, or 2%, to $123.3 million during 2016 from $121.1 million in 2015.

Diluted EPS attributable to stockholders for 2016 was $0.85, a 33% decrease compared to $1.27 in 2015. This decrease is primarily due to non-recurring events in both years. Diluted adjusted EPS attributable to stockholders (non-GAAP measure) increased 2% to $1.15 per share in 2016 from $1.13 per share in 2015.

Balance sheet analysis as at and for the 12 months ended December 31, 2016

Working capital margin, calculated as working capital divided by revenues, declined 510 basis points to 22.1% in 2016 from 27.2% in 2015. This decrease is primarily due to a decrease in inventory by $30.0 million combined with an increase in revenues by $50.5 million year-over-year. The decrease in inventory is primarily due to a higher volume of underwritten business at the end of 2015 compared to the end of 2016, where the majority of the 2015 inventory was sold at the first large auction of 2016, the February Orlando auction. Working capital intensity7 (non-GAAP measure) improved by 570 basis points, to -8.9% in 2016 from -3.2% in 2015.

Return on average invested capital is calculated as net income attributable to stockholders divided by average invested capital. The Company measures average invested capital over a trailing 12-month period by adding the average long-term debt over that period to the average stockholders' equity over that period. Return on average invested capital decreased 820 bps to 8.8% during 2016 from 17.0% in 2015. This decrease is primarily due to a $239.8 million, or a 30%, increase in average invested capital year-over-year, which was primarily the result of the issuance of $500 million of unsecured senior notes (the "Notes") in the fourth quarter of 2016. Also contributing to the decrease in return on average invested capital in 2016 compared to 2015 was a $44.4 million, or 33%, decrease in net income attributable to stockholders. Return on invested capital ("ROIC")8 (non-GAAP measure) decreased 330 bps to 11.8% during 2016 from 15.1% in 2015.

ROIC excluding escrowed debt9 (non-GAAP measure) increased 40 bps to 15.5% during 2016 from 15.1% in 2015.

7

The Company's balance sheet scorecard includes the performance metric, working capital intensity, which is a non-GAAP measure. The Company believes that comparing working capital intensity on a trailing 12-month basis to different financial periods provides useful information about how efficiently the Company converts revenue into cash. The lower the percentage, the faster revenues are converted into cash. The Company calculates working capital intensity as trade and other receivables plus inventory and advances against auction contracts less auction proceeds payable and trade payables, divided by revenues. Working capital intensity is reconciled to the most directly comparable GAAP measures in the Company's consolidated financial statements under "Non-GAAP Measures" below.

8

ROIC is a non-GAAP financial measure that the Company believes, by comparing on a trailing 12-month basis for different financial periods provides useful information about the after-tax return generated by its investments. The Company's balance sheet scorecard includes the performance metric, ROIC. ROIC is also an element of the performance criteria for certain PSUs the Company granted to its employees and officers in 2013 and 2014. The Company calculates ROIC as net income attributable to stockholders excluding the effects of adjusting items divided by average invested capital. Average invested capital is a GAAP measure calculated as the average long-term debt (including current and non-current portions) and stockholders' equity over a trailing 12-month period. ROIC is reconciled to the most directly comparable GAAP measures in the Company's consolidated financial statements under "Non-GAAP Measures" below.

9

ROIC excluding escrowed debt is a non-GAAP financial measure that the Company believes, by comparing on a trailing 12-month basis for different financial periods provides useful information about the after-tax return generated by its investments by removing the impact of the issue of the Notes, which are currently held in escrow. While the Notes are in escrow and not accessible by the Company, they are not contributing to the generation of net income. The Company believes that by adjusting debt to remove funds it does not have access to, it is providing more accurate information about the after-tax return generated by its investments. The Company calculates ROIC excluding escrowed debt as adjusted net income attributable to stockholders (non-GAAP measure) divided by adjusted average invested capital (non-GAAP measure). The Company calculates adjusted average invested capital (non-GAAP measure) as the adjusted average long-term debt (non-GAAP measure) and average stockholders' equity over a trailing 12-month period. The Company calculates adjusted average long-term debt (non-GAAP measure) as the average of adjusted opening long-term debt (non-GAAP measure) and adjusted ending long-term debt (non-GAAP measure). Adjusted opening long-term debt (non-GAAP measure) and adjusted ending long-term debt (non-GAAP measure) are calculated as opening or ending long-term debt, as applicable, as reported in the Company's consolidated financial statements reduced by long-term debt held in escrow. ROIC excluding escrowed debt is reconciled to the most directly comparable GAAP measures in the Company's consolidated financial statements under "Non-GAAP Measures" below.

Dividend Information Quarterly Dividend

On January 23, 2017, the Company declared a quarterly cash dividend of $0.17 per common share payable on March 3, 2017 to shareholders of record on February 10, 2017.

Operational Review Online Statistics

During 2016, the Company attracted record annual bidder registrations and sold approximately $2.1 billion of equipment, trucks and other assets to online auction and EquipmentOne customers. This represents an 8% increase compared to the $1.9 billion of assets sold online during 2015.

During the fourth quarter of 2016, the Company attracted record fourth quarter online bidder registrations and sold approximately $524.7 million of equipment, trucks and other assets to online auction bidders and EquipmentOne customers. This represents a $25.3 million, or 5%, decrease in online transactions compared to the $550.0 million of assets sold online during the fourth quarter of 2015.

EquipmentOne Activity

During 2016, EquipmentOne sold more than $148.0 million of equipment and other assets on behalf of customers and saw a 9% increase in revenues compared to 2015. During the fourth quarter of 2016, EquipmentOne sold more than $40.6 million of equipment and other assets on behalf of customers and saw a 9% increase in revenues compared to the fourth quarter of 2015.

Auction Activity

During the fourth quarter of 2016, Ritchie Bros. conducted 71 unreserved industrial auctions in 15 countries throughout North America, Central America, Europe, the Middle East, Australia, and Asia. Auctions highlights during the quarter include:

On December 8-9, 2016, more than 4,500 equipment items, trucks and other assets were sold at the Edmonton, Alberta auction, for CA$66+ million (US$50+ million).

On November 30 – December 1, 2016, more than 4,950 assets were sold at the Fort Worth, Texas auction, for US$40 million.

On November 9-10, 2016, more than 4,200 equipment items, trucks and other assets were sold at Houston, Texas auction, for US$43+ million.

At the four-day Edmonton, Alberta auction, held on October 25-28, 2016, more than 8,000 assets were sold for CA$129+ million (US$96+ million).

There are currently 142 unreserved auctions on the Ritchie Bros. auction calendar at www.rbauction.com, including auctions in North America, Europe, the Middle East, Australia, New Zealand, and Asia.

Corporate Development Updates

Announced Acquisition of IronPlanet

On August 29, 2016, Ritchie Bros and IronPlanet, a leading online marketplace for used heavy equipment and other durable asset sales, jointly announced the companies have entered into an agreement under which Ritchie Bros. will acquire IronPlanet for approximately US$758.5 million, subject to customary closing adjustments and conditions.

As previously disclosed, the transaction remains subject to expiration or termination of the prescribed waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the "HSR Act"). As anticipated, on December 15, 2016, the United States Department of Justice (the "DoJ") provided Ritchie Bros. with a second request for information as part of their standard review procedure under the HSR Act. The effect of the second request is to extend the waiting period imposed by the HSR Act until 30 days after Ritchie Bros. and IronPlanet have substantially complied, unless that period is extended voluntarily by the parties or terminated sooner by the DoJ. While the closing of the transaction is subject to the DoJ review and customary closing conditions, the Company still believes the acquisition is likely to close before the end of the second quarter of 2017.

Ritchie Bros. and IronPlanet are actively engaged in planning the integration of our businesses, to ensure a swift and seamless business combination following the close of the acquisition.

Acquisition of Kramer Auctions

On August 1, 2016, Ritchie Bros. acquired the business of Kramer Auctions, a leading Canadian agricultural auction company with exceptionally strong customer relationships in central Canada. This acquisition is expected to significantly strengthen Ritchie Bros.' penetration of Canada's agricultural sector and add key talent to our Canadian Ag sales and operations team.

Operating for more than 65 years, Kramer Auctions has established a leading market position in Alberta, Saskatchewan and Manitoba as a premier agricultural auctioneer, offering both on-the-farm and on site live auctions for customers selling equipment, livestock and real-estate in the agricultural sector. The family-owned and operated business has developed deep, loyal customer relationships, which have been developed over three generations of management by the Kramer family. The business operates approximately 75 on-the-farm auctions, four on site auctions, and eight livestock (Bison) auctions each year, and sold more than CA$60 million of agricultural equipment, real-estate and other assets in the last year. Like Ritchie Bros. Auctioneers' auctions, Kramer Auction sales are conducted on an unreserved basis.

Completion of US$1 billion of New Credit Facilities

On October 27, 2016, the Company announced the closing of a new five-year credit agreement totaling US$1.0 billion with a syndicate of lenders comprising (1) multicurrency revolving facilities of up to US$675 Million (the "Revolving Facilities"), and, (2) a delayed-draw term loan facility of up to US$325 Million to finance the previously announced acquisition of IronPlanet (the "Delayed-Draw Facility" and together with the Revolving Facilities, the "Facilities").

The Facilities will remain unsecured until the closing of the IronPlanet acquisition, after which the Facilities will be secured by assets of Ritchie Bros. and certain of its subsidiaries in Canada and the United States. The Facilities are expected to become unsecured again after the IronPlanet acquisition, once Ritchie Bros. meets specified credit ratings or leverage ratio conditions. Ritchie Bros. intends to pay down debt levels following the close of the IronPlanet acquisition with expected cash flows, which should facilitate the release of the security on the debt. The Company consistently generates free cash flows in excess of net income as it processes cash flows relative to its auction proceeds, not simply its revenues.

In conjunction with this refinancing, Ritchie Bros. terminated approximately US$600 million of its pre-existing revolving bi-lateral credit facilities and private notes to provide the Company with more suitable covenants and financial flexibility. US$6.8 million of debt extinguishment costs were recognized in the fourth quarter in relation to the early termination of the private notes.

Issuance of US$500 million of Notes

On December 21, 2016, Ritchie Bros. completed an offering of $500 million of Notes, due 2025. Ritchie Bros. intends to use the net proceeds, together with proceeds from its delayed-draw term loan and cash on hand or available under its revolving facilities, to fund the consideration payable in the previously announced acquisition of IronPlanet and related fees and expenses. The gross proceeds from the offering, together with additional amounts from cash on hand or borrowings from our existing credit facilities to prefund accrued interest, will be held in an escrow account pending the consummation of the IronPlanet acquisition.

The Notes were issued at par, with a maturity date of January 15, 2025. The Notes accrue interest at a rate of 5.375% per year, with interest to be paid semi-annually on each January 15 and July 15, commencing January 15, 2017.

Announcing retirement of Randy Wall

Randy Wall, President of Ritchie Bros.' Canadian operations and a long-time executive of the Company, has indicated his intention to retire during the second quarter of 2017. Randy has been a valued and highly-experienced member of Ritchie Bros.' executive team for many decades, and with the exception of a 5-year hiatus related to his earlier retirement before re-joining the Company full-time, has worked with Ritchie Bros. for nearly 29 years. The Company is currently considering internal candidates for its succession plan, and will provide an update on future leadership appointments for the Canadian business once a decision has been made.

Management Appointments

The Company is pleased to announce that Karl Werner has been promoted to President, International, to oversee all regions outside of North America and Latin America. Mr. Werner was most recently Chief Operational Support and Development Officer and Managing Director of the Middle East, though Karl has held progressively more senior roles throughout his 20-year career with Ritchie Bros. His new role will be effective April 1, 2017.

The Company is also pleased to announce the promotion of Kieran Holm to SVP, Operational Excellence & Efficiencies. In this new role, Mr. Holm will be responsible for driving cost reductions through implementing global procurement and sourcing strategies, delivering site efficiencies through best in class benchmarking, and transferring best practices while proactively optimizing the site network, focusing initially on North America. Most recently, Kieran was VP and Managing Director, Asia Pacific, but has held numerous roles within Ritchie Bros. in sales, marketing, and leadership capacities during his 13 years with the Company. Kieran's new role will be effective April 1, 2017.

Sharon Driscoll, CFO, has been given an expanded scope of responsibilities. In addition to her current role, she will now Chair the board of Ritchie Bros. Financial Services and also oversee all Ritchie Bros. properties and real estate assets.

Closure of Beijing and Panama auction sites; new strategic direction for Japan

Ritchie Bros. is currently evaluating the returns generated at each of the permanent and regional auction sites we operate, to ensure each site (and related site capital investments) are generating returns that meet predetermined targets. As a result of the analysis completed to date, it was determined that both the Beijing and Panama sites would be closed. The lease for the Beijing site was early-terminated in November 2016. The company is currently negotiating exiting its lease for its Panama site, though no future auctions are expected to be held there. In China, Ritchie Bros. will continue to offer offsite auctions and other equipment sales channels through its sales team based there. In Panama, the Company will consider holding offsite auctions as opportunities arise.

Ritchie Bros. established a fully owned site in Narita, Japan, in 2010 to run live auctions. Unfortunately, the site had limited success offering Ritchie Bros.' traditional live, unreserved auction model due to both cultural factors and market dynamics in Japan. Over the last two years, Ritchie Bros. has studied the market comprehensively, built strong local relationships and tested different business models. The Company has come to the conclusion that its biggest opportunity in Japan is to position it as a "source" market for high quality used equipment that can be exported throughout the Asia Pacific region and the Middle East. Ritchie Bros. also believes the most efficient way to serve the domestic Japanese market is primarily through digital channels, while leveraging key Original Equipment Manufacturer relationships. Consequently, the Company will commence an exploration of exiting its Narita, Japan auction site at an appropriate time to maximize value.

Q4 2016 Earnings Conference Call

Ritchie Bros. is hosting a conference call to discuss its financial results for the quarter ended December 31, 2016, at 8:00 am Pacific time / 11:00 am Eastern time / 4:00 pm GMT on February 21, 2017. A replay will be available shortly after the call.

Conference call and webcast details are available at the following link: https://investor.ritchiebros.com

Construction Equipment Guide

470 Maryland Drive

Fort Washington, PA 19034

800-523-2200

Construction Equipment Guide covers the nation with its four regional newspapers, offering construction and industry news and information along with new and used construction equipment for sale from dealers in your area. Now we extend those services and information to the internet. Making it as easy as possible to find the news and equipment that you need and want.

Contents Copyrighted 2024, by Construction Equipment Guide, which is a Registered Trademark, registered in the U.S. Patent Office. Registration number 0957323. All rights reserved, nothing may be reprinted or reproduced (including framing) in whole or part without written permission from the publisher. All editorial material, photographs, drawings, letters, and other material will be treated as unconditionally assigned for publication and copyright purposes and are subject to Construction Equipment Guide’s unrestricted right to edit and comment editorially. Contributor articles do not necessarily reflect the policy or opinions of this publication.

Read our privacy policy here.

Mastodon