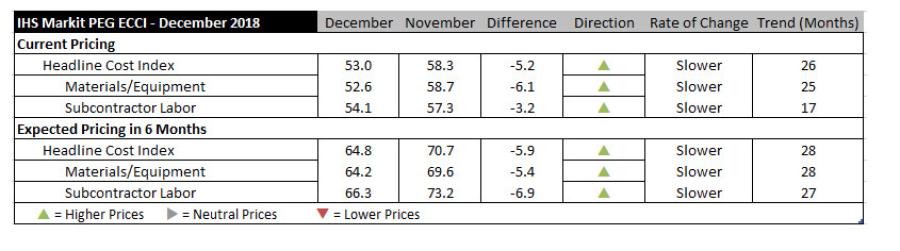

Construction costs increase continued to slow in December, according to IHS Markit and the Procurement Executives Group (PEG). The current headline IHS Markit PEG Engineering and Construction Cost Index registered 53.0 this month, the lowest index figure for 2018. Although prices are still rising (the index remains above 50 for both materials and labor) increases have been less widespread in the last two months.

Materials and equipment prices rose in December, however the index figure dropped once again from 58.7 in November to 52.6 in December. The index figure for materials and equipment has not been this low since July 2017. Price increases were recorded in 6 of the 12 subcomponents in December, heat exchangers, turbines and ready-mix concrete showed flat pricing, while fabricated structural steel, carbon steel pipe and alloy steel pipe experienced price declines. Steel and pipe prices began to drop after a 15-month stretch of rising prices.

"Steel prices have a downward bias in the United States, Europe and Asia," said John Anton, director, pricing and purchasing at IHS Markit. "Demand is not providing support and prices in mid-2018 were above equilibrium. Steel is moving from a sellers' market to a buyers' market; most products should hit their floor in the first half of 2019."

Current subcontractor labor price increases also were not widespread in December. The index, although still in expansion territory, dipped to 54.1 in December from 57.3 in November. Labor costs were flat in the U.S. Northeast and Midwest but continued to increase in the U.S. South and West. In Canada, the Eastern part of the country registered higher labor costs while labor costs remained flat in the West.

The six-month headline expectations for construction costs index reflected increasing prices for the 28th consecutive month. The materials/equipment index slipped once more but stayed in expansion territory with a reading of 64.2. Expectations for future price increases were widespread, with all material indexes resting above 55.0. Price expectations for sub-contractor labor stayed positive at 66.3. Labor costs are expected to rise in all regions of the United States and Eastern Canada; they are expected to remain flat in Western Canada.

In the survey comments, respondents indicated a tight labor market for all skilled trade workers.

To learn more about the IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, visit click here.